Setting S.M.A.R.T. Goals: A Simple How-To Guide

Setting S.M.A.R.T. Goals: A Simple How-To Guide

Welcome to the world of smart financial goal setting! Whether you're looking to pay off debt, save for a vacation or a wedding, or build an emergency fund, having a well-structured plan can make all the difference. In this article, we'll introduce you to S.M.A.R.T. goals, a technique that is a powerful framework to help you achieve your financial dreams.

Each letter in the S.M.A.R.T. acronym represents a key element in setting goal: Specific, Measurable, Achievable, Relevant, and Time-bound. We'll break down each element and provide real-life examples to show you how to apply the S.M.A.R.T. technique effectively.

So let's dive in and learn how to turn your financial goals into concrete plans using the S.M.A.R.T. approach. Get ready to take charge of your financial future!

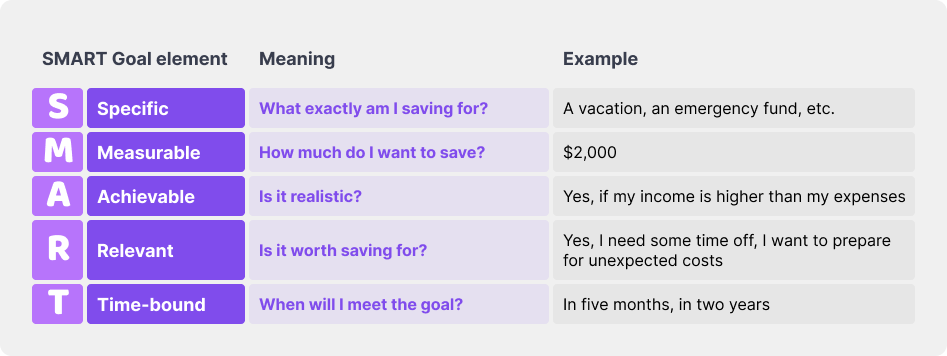

Here's What Each Element of the S.M.A.R.T. Acronym Means

Specific, Measurable, Achievable, Relevant , and Time-bound. That is each of the individual acronyms of S.M.A.R.T. technique. It was developed by George Doran, Arthur Miller and James Cunningham in their 1981 article “There's a S.M.A.R.T. way to write management goals and objectives” .

They described it as a framework that can be used in business, project management, and personal development to effectively set and achieve goals. When you apply the S.M.A.R.T. framework to your personal finances, it can help you set and achieve specific financial goals in a structured and effective way. Let's learn how!

Specific

Your financial goals should be clearly defined and specific. Instead of a vague goal like "save money," make it more specific, such as "save $5,000 for a down payment on a house" or "pay off $10,000 in credit card debt." Being specific helps you know exactly what you're working toward.

Measurable

Make sure your financial goals are measurable, meaning you can track your progress and determine when you've achieved them. If your goal is to save money, specify how much and by when. For example, "save $500 per month for 12 months."

Achievable

Ensure that your financial goals are realistic and achievable given your current financial situation and resources. Setting a goal to save a million dollars in a year when you're earning an average income might not be achievable. Instead, set a goal that challenges you but is within reach, such as "increase my savings by 10% this year."

Relevant

Your financial goals should be relevant to your overall financial well-being and life objectives. They should align with your values and priorities. For example, if homeownership is a priority for you, a relevant goal might be "save for a down payment on a home."

Time-bound

Set specific timeframes for your financial goals. Having a deadline creates a sense of urgency and helps you stay focused. For example, "pay off my student loans in five years" or "build an emergency fund of $10,000 within 18 months."

S.M.A.R.T. Goals Example

Let's consider an example of someone using the S.M.A.R.T. technique for setting a personal financial goal. In this scenario, we'll follow Malik, a recent college graduate who is determined to pay off his student loans responsibly and efficiently.

Malik's goal is to pay off his student loans. He has $30,000 in student loan debt from his undergraduate degree, and he wants to eliminate this debt as soon as possible. His specific goal is to pay off his entire $30,000 student loan balance.

Malik's goal is easily measurable because he has a specific dollar amount in mind. He can track his progress by checking his loan balance and watching it decrease over time.

To determine if this goal is achievable , Malik assesses his financial situation. He has just started a full-time job with a $45,000 annual salary, and his monthly take-home pay is around $3,500. After accounting for living expenses, he believes he can allocate an extra $500 per month toward his student loans. This means he can allocate $6,000 per year to loan repayment. If he maintains this pace, it will take him approximately five years to pay off his loans, which is a realistic timeframe.

Paying off his student loans is highly relevant to Malik's financial well-being and long-term goals. It will free up his monthly budget, improve his credit score, and allow him to save and invest more for his future. Plus, it aligns with his values of financial responsibility and independence.

Malik sets a clear time frame for achieving his goal. He aims to pay off his student loans in five years. He calculates that if he pays $6,000 annually, he will have paid off $30,000 in five years.

How to apply S.M.A.R.T. goals in Wallet by BudgetBakers

You can use Wallet by BudgetBakers to make reaching your goals even easier. By setting budgets and planned payments in the app, you can set specific goals along with timeframes, and monitor your successes with the tracking feature.

Syncing all your bank and neo-bank accounts with Wallet will help you factor all your income and expenses into your goals.

Give it a try - Start your S.M.A.R.T. journey today!